10 Reasons Why K–12 School Districts Fail Financial Audits (and How to Fix Them)

Each year, nearly one in four K–12 school districts fail some portion of their audit. What happens when a district fails an audit? The consequences range from compliance findings and reputational damage to state intervention, legal exposure, and in serious cases, significant financial loss tied to fraud or misappropriation of funds. And yet most of these failures trace back to the same fixable problems.

Are you concerned about potential gaps in your district’s internal controls? Take our 5-minute School District Fraud Assessment to identify high-risk areas before your next audit.

KEV Group’s analysis of publicly reported fraud cases shows that, since 2024, K–12 schools across North America have lost more than $49 million to fraud — with 68% of incidents occurring at the school level, where financial controls are typically weakest.

So why do so many districts stumble? And more importantly, how can they prevent it?

If you’re looking for the practical follow-through — what to actually do month by month — the school audit checklist for K-12 finance teams covers exactly that.

To answer that, we spoke with Dava Watson, who has over 20 years of experience in K–12 finance, including serving as an internal auditor at Austin ISD, where she oversaw 130+ schools. Dava shared insight into the ten most common — and completely fixable — reasons districts fail audits.

Key Takeaways

- Financial audit deficiencies are widespread and costly. Nearly one in four K–12 districts fail some portion of their audit, often leading to reputational damage, compliance issues, and financial losses.

- Weak internal controls and outdated processes are major drivers. Lack of continuous monitoring, manual reconciliations, and legacy systems leave districts exposed to errors and audit findings.

- Poor cash handling and documentation increase risk. Excessive cash use, delayed deposits, missing receipts, and weak documentation create red flags for auditors.

- Compliance gaps extend beyond bookkeeping. Issues like unauthorized vendors, unposted transactions, and misuse of activity funds reflect deeper operational weaknesses.

- Audit readiness requires everyday practices. Audit success isn’t seasonal, it’s built on strong controls, standard procedures, and regular training.

- Purpose-built systems help close gaps. Investing in integrated K–12 finance tools that unify accounting, payments, and reporting can strengthen audit trails and reduce risks.

Audit Findings: Understanding Severity Levels

| Finding Type | Definition | Severity | K-12 Example | Audit Impact |

|---|---|---|---|---|

| Control Deficiency | Flaw in design or operation that doesn’t allow prevention/detection of errors. | LOW | A single teacher forgot to sign a $20 field trip deposit slip. | Mentioned in a Management Letter. |

| Significant Deficiency | More severe than a deficiency, but less than a material weakness. | MEDIUM | Multiple schools failing to use approved vendors across the district. | Reported to the Board; signifies a trend of weak oversight. |

| Material Weakness | Reasonable possibility of material misstatement not being prevented. | HIGH | One person collects cash, records it, and reconciles the bank. | Publicly disclosed in financial statements; high fraud risk. |

Source: Generally Accepted Auditing Standards (GAAS) applied to K-12 finance.

1. Weak internal controls

Some districts have eliminated internal audit teams, assuming external audits will suffice. But this in itself is a risk. External auditors only test small samples. They simply can’t look at everything across a district. Internal auditors go deeper — reviewing procurement, IT systems, risk management, and operational efficiency — exactly where most audit failures originate.

Without continuous controls, small errors can snowball into costly findings.

“I’ve noticed a lot of districts are getting rid of their internal audit departments because they know that the external audit is just going to look at a very small sample and they’re going to do a balance sheet audit. Internal audits really dig deeper. They’re going to make sure all checks and balances are in place.

– Dava Watson

💡Pro Tip: Maintain dedicated internal audit staff

Even one auditor can drastically reduce risk. Larger districts like Austin ISD employed ten auditors — a cost that paid for itself by preventing major financial disasters.

2. Excessive cash handling

Cash is still common in many districts — and it’s the riskiest form of payment. According to KEV Group’s research, 62% of school-level fraud cases involve cash.

From athletics concessions to fundraiser proceeds, cash passes through many hands with minimal oversight, and every physical touchpoint increases audit risk. And when students bring cash to school, it invites the possibility of money being lost or stolen.

💡Pro Tip: Implement strong cash handling protocols

To limit risk and strengthen audit readiness, districts can follow cash-handling best practices such as:

- Depositing all cash “intact” (the exact bills and coins received)

- Using digital payment systems to minimize the amount of cash collected

- Documenting every cash transaction with clear, traceable receipts

3. Delayed deposits

What some staff might see as harmless “borrowing” is actually theft, and it’s one of the most common audit failure examples. In some districts, bookkeepers may delay deposits because they’re short on cash before payday — taking money from collections with the intent to “replace it later” and temporarily covering the gap with a personal check.

This creates misleading records, hides theft, and makes it difficult to track whether funds were ever fully deposited. It also signals to auditors that internal controls are weak, increasing scrutiny across the entire school.

“If you’ve got more than $500 in cash, it should be deposited daily. Waiting until payday is borrowing. And borrowing is stealing.”

– Dava Watson

💡Pro Tip: Implement non-negotiable deposit timeframes

Districts should set clear expectations that:

- Deposits over $500 are made daily

- Deposits under $500 are made within two business days

- ‘Borrowing’ from deposits is never allowed

4. Missing receipts

Audit trails fall apart when receipts aren’t issued consistently. Teachers sometimes skip receipts for “small” collections. But auditors don’t see “small” — they see non-compliance.

Every cash collection needs a clear paper trail. Even a single missing receipt signals a breakdown in controls and prompts auditors to dig deeper into additional transactions.

💡Pro Tip: Require documentation for every transaction, no matter how small

Whether through formal receipts or simple class rosters with student names and amounts collected, every dollar must be documented. As Dava notes: “It could be your class roster and you could just write $10 by the kid’s name.”

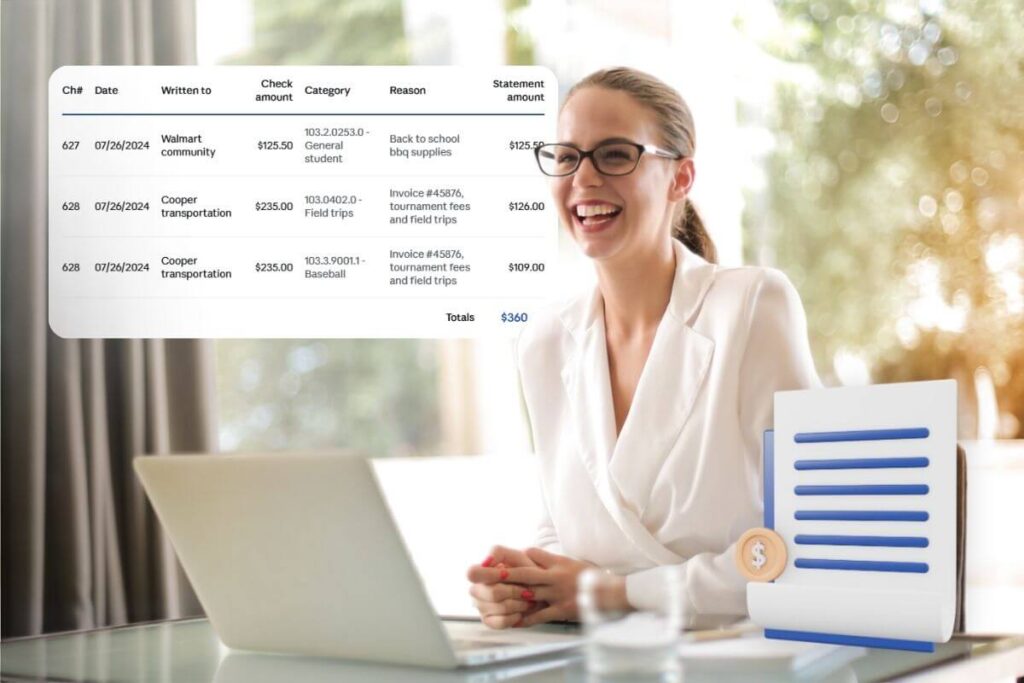

5. Manual reconciliations

Manual reconciliations are one of the most common reasons districts fail financial audits. They’re slow, error-prone, and often misunderstood. Bookkeepers may not fully grasp complex account structures, which leads to missed items, incorrect balances, and delays — all of which raise red flags for auditors. Manual processes are also far easier to manipulate, making it difficult to distinguish honest mistakes from deliberate concealment.

“We had probably 25% of our districts failing their audits, and for the most part it was just due to reconciliations… more than three late ones in a year was an automatic failure of your activity fund audit.”

– Dava Watson

💡Pro Tip: Use guided reconciliation tools to reduce errors and delays

School accounting software with guided reconciliation helps bookkeepers quickly clear transactions, flag discrepancies, generate accurate month-end reports, and lock periods — reducing mistakes, improving timeliness, and strengthening audit readiness.

6. Unauthorized vendors

When schools bypass district-approved vendors, they open the door to conflicts of interest, inflated pricing, and fraud risk. While choosing an unapproved vendor may seem harmless, it undermines procurement rules designed to protect districts from misuse of funds.

Common risks include hiring family members at premium rates, double-billing through external organizations, or issuing payments with no formal bid or verification process.

“Every vendor in a school district has to be approved. You can’t just go out and use your own vendor.”

– Dava Watson

💡Pro Tip: Only use approved vendors

Ensure your K–12 finance system restricts users from adding or selecting unauthorized vendors. Limiting payments to vetted, district-approved vendors helps maintain proper audit trails, ensures accurate 1099 reporting, and reduces the risk of fraud or conflict of interest.

7. Unposted transactions

Unposted or manipulated transactions can hide serious issues for months — or even years. In manual or paper-based systems, it’s far too easy to create fake journal entries, add “ghost” transactions to unmonitored categories, alter digital bank statements, or use personal checks to temporarily cover stolen cash.

These tactics are classic signs of fragmented systems with weak controls. Auditors know this, which is why unexplained adjustments, inconsistent entries, or transactions that never clear are among the first areas they investigate.

💡Pro Tip: Use systems with immutable transaction records

Choose financial tools that prevent users from altering or backdating entries and that record every action with a complete audit trail. Immutable records make suspicious activity easier to detect — and much harder to conceal.

8. Misuse of activity funds

School activity funds belong to the students who raised them — not the staff, not the school, and not future classes. Yet auditors commonly find funds being held for years, redirected to unrelated expenses, or treated like discretionary accounts by sponsors.

Money raised in a given school year must benefit the students who raised it that same year. And school activity funds cannot be transferred between groups. If the choir has money but the band does not, the choir’s funds cannot be used for the annual school band trip — even if both fall under the fine arts umbrella.

Misuse of activity funds is one of the most frequent and easily preventable compliance failures.

💡Pro Tip: Create clear student activity fund guidelines

Regularly review activity account balances to ensure funds are being spent appropriately and in a timely manner. Establish and enforce policies that prevent year-over-year rollover and transfers between unrelated groups.

9. Weak documentation

Missing, inconsistent, or altered documentation is one of the fastest ways to escalate a basic compliance review into a full investigation. Auditors look closely to identify red flats and patterns — a few missing signatures, unexplained edits, or recurring outstanding items often signal deeper issues.

Common triggers include purchase orders without required approvals, bank statements that appear altered, deposits carried over month after month, or mismatches between receipts and recorded amounts. With the ease of editing PDFs today, auditors are increasingly vigilant about verifying the authenticity of documents.

“If you find one purchase request missing a signature, okay. If you find three out of ten missing, then they’re going to go look at all of them.”

– Dava Watson

💡Pro Tip: Use digital documentation with audit trails

Adopt systems that store unalterable digital records, capture all required approvals, and maintain a complete timestamped history for every transaction. Reliable digital documentation strengthens audit readiness and eliminates the guesswork often found in paper-based school audit processes.

10. Outdated systems and processes

Many districts still rely on spreadsheets, paper receipts, or unauthorized personal payment apps like PayPal, Venmo, or Cash App. These tools can create blind spots with little to no oversight, and they’re a major reason school-level fraud so often goes undetected.

Legacy processes also make it difficult to track documentation, monitor transactions, or enforce consistent approval workflows. When systems don’t talk to each other — or don’t provide any audit trail at all — districts are left exposed.

💡Pro Tip: Invest in a purpose-built K–12 finance solution

Look for a school finance platform designed specifically for K–12 — one that unifies accounting, payments, and reporting in a single system, reduces reliance on cash, and provides the robust school audit controls districts need.

What audit-ready school districts do differently

Leading districts don’t wait for audit season — they build audit readiness into everyday operations. Instead of reacting to findings after the fact, they embed strong financial practices throughout the year by:

- Implementing real-time reconciliation workflows that prevent late or missed reconciliations

- Standardizing categories, forms, and naming conventions across all schools to eliminate confusion

- Training all staff on audit hygiene and early risk indicators, making everyone part of the first line of defense

- Building a 12-month school audit checklist that distributes preparation rather than cramming at year-end

- Investing in integrated financial systems that reduce manual work and create complete, end-to-end audit trails

“A lot of people think auditors are there to ‘get you’ but they’re not. They want to ensure schools look good, stay compliant, and keep taxpayer funds safe.”

– Dava Watson

Next steps

Audit failures aren’t inevitable — they’re the predictable outcome of weak controls, limited visibility, and the absence of dedicated K–12 finance systems. With the right processes and platform in place, districts can protect every dollar and ensure compliance all year long.

If your district is ready to strengthen compliance, reduce risk, and modernize school-level financial management, connect with a school finance expert to see how we can help.

Get K–12 finance insights in your inbox

Recommended For You